Market Review

The benchmark S&P 500 index closed the 1st quarter down 4.6% to break a run of three consecutive quarterly gains. Index returns were modest but largely positive thru most of February, but events in the Middle East made for a saw-toothed downward path to the eventual quarterly return. Geopolitical events will likely dominate investors’ recollection of the first three months of the year, but companies continued to report strong financial results from the preceding quarter. Fourth quarter earnings rose almost 13½% versus the prior year and topped consensus projections by almost 7%. Revenue surprised by almost 2% to post a growth rate slightly over 9%. Analysts anticipate that earnings grew almost 11% during the 1st quarter and will expand by almost 14% over the course of the year. The Federal Reserve (“the Fed”) opted to leave their policy rate unchanged at each of their two 1st quarter meetings, largely as expected after three rate cuts during the 4th quarter to take their policy stance more toward neutral footing. The statement after the March meeting indicated that the potential impact of the Middle East conflict on both inflation and economic growth influenced the decision to make no change to monetary policy.

The Economy

The U.S. economy posted a 0.7% growth rate during the 4th quarter, largely weighed on by a lengthy government shutdown that curtailed federal spending during much of October. Consumption, however, rose by a quite respectable 2.0%. Per the Federal Reserve Bank of Atlanta’s GDPNow model estimate, 1st quarter economic growth has risen by around 2%, which is slightly below the economist community’s call for slightly stronger growth at 2.3%. Even before the March spike in oil prices, the Fed’s preferred Core Personal Consumption Expenditures Deflator had edged up to slightly more than 3% year-over-year in January v. the Central Bank’s stated 2% target. Forecasters anticipate that U.S. G.D.P. will expand by an above-trend 2.4% during 2026, but the repercussions of higher oil prices on consumer and corporate purse strings may influence that outcome. While unemployment claims remain at low levels that indicate job stability, non-farm payrolls fell by 92,000 during February and have decreased in five of the last nine months, raising concerns about a lack of job growth. However, Fed members polled at the March meeting expect that the unemployment rate will remain steady through 2026.

Equity Markets

The S&P 500 topped three sectors during the 1st quarter, besting Healthcare, Tech and Financials by sizeable margins, but trailed several other sectors noteworthy gaps. One takeaway for investors is the unusually wide dispersion in returns across sectors, with Energy (+25.8%) gaining well over 20% and Financials (-9.8%) dropping close to 10%. As has been common in recent quarters, artificial intelligence (“A.I.”) remains a key market influence. Energy was already leading the way by some distance before events heated up in the Middle East, as the data centers that house A.I. infrastructure need enormous amounts of electricity to power their operations, and the most expedient source of that power is natural gas-powered turbine generators, which are increasingly being situated adjacent to data centers and the natural gas infrastructure that fuels them. Both the suppliers of fuel and power generation companies stand to benefit from this setup. Industrials (+4.3%) will play their part in the A.I. infrastructure buildout by constructing the data centers, connecting power producers to power consumers and strengthening the aging power grid. Companies in the sector will also provide the cooling apparatuses to keep the computer equipment inside data centers cool enough to operate at optimal levels. Materials (+9.3%) companies will supply the building supplies for those data centers. Real Estate (+1.9%) posted respectable returns for the quarter as the sector contains some of the largest data center landlords. Communication Services (-7.1%) and Tech (-9.2%) both suffered from the same overhang, as investors question the eventual returns on huge up-front investments in A.I. infrastructure. As of recent updates, the major Cloud service providers who facilitate A.I. and accelerated computing, including both Alphabet (Communication Services) and Microsoft (Tech), plan to invest over $600 billion during 2026. Financials suffered as investors began to worry about credit quality for certain higher-risk companies who need to borrow in privately negotiated markets rather than in the publicly-traded bond market. The Consumer (-3.3%) sector pulled back sharply during March, flipping from positive to negative returns, as investors projected the impact of energy-driven inflation on overall household spending power. Healthcare (-5.3%) stocks also reversed into negative territory during March, as aggressive policy rhetoric about lowering pharmaceutical costs and shortening patent protection weighed on the sector.

Long-Term View

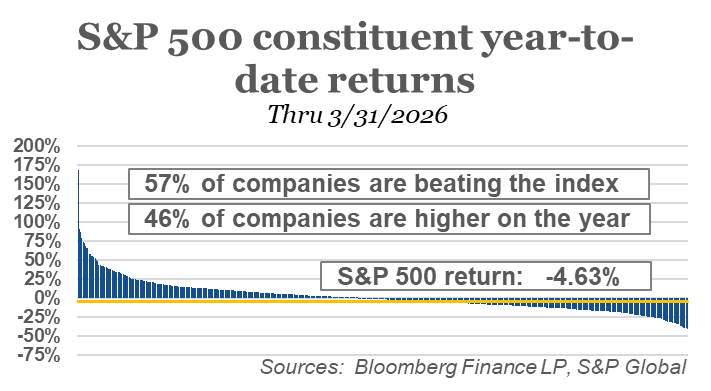

Equity strategists entered the year bullish about market prospects for a 4th straight year of solid gains in 2026 and largely retain that positive outlook. Over 40% of S&P 500 component companies have posted gains year-to-date, despite the index being down over 4% [see chart], illustrating that there are attractive investment opportunities in most any market environment. Forecasts still indicate that corporate earnings will grow quite strongly this year, with growth accelerating as the year moves into its 2nd half. Analysts modeling business prospects for individual companies continue to revise earnings and revenue estimates upward, which should eventually bode well for those stocks if those estimates become reality. The events of the past month or so present some risks and some uncertainty that investors would be wise to monitor, but largely discount in the near-term when it comes to making changes to investment strategies designed to weather such storms without impacting expected cash flows. Past episodes show that financial markets can quickly move past the tumult of geopolitical events and resume course, even in the face of larger-scale conflicts. Volatility, however, is the toll investors pay for the handsome gains that can be on offer, even if that means weathering three or four 5% pullbacks during the average year. With history as a guide, investors who ride out the volatility tend to fare better than investors who move to the sidelines.